U. S. markets, in particular the stock markets and petroleum markets, have, with considerable help from the Federal Reserve, made a stunning recovery from the 2008 price plunge. Does this mean that we are in a position where we could experience another hefty price drop? Perhaps, so it’s relevant that we ponder the lessons learned five years ago and consider a couple of applicable hedging strategies.

Consumer Defaults

In the 2008/2009 heating season, arguably the most disastrous outcome experienced by heating oil retailers was widespread consumer defaults on fixed price purchase commitments. The problem here is that customers committed to buy heating oil at a fixed price and the dealer in turn committed to a lower fixed price hedge, theoretically locking in an acceptable margin. When prices went into the tank and consumers refused to take delivery of high-priced heating oil, the retailer was compelled by suppliers to buy high-price contract gallons with no opportunity to resell these gallons at a corresponding high retail price, resulting in inadequate, sometimes even negative, margins.

In response, dealers consulted with their attorneys and tightened up their price protection contracts, so that they could more successfully pursue legal action against non-compliant fixed price customers. Many also resolved that going forward, they will offer only capped price contracts. The logic behind this decision is undeniable. A lack of price protection is great if prices are falling, but the unprotected consumer is vulnerable to price increases. A fixed price contract protects against rising prices, but the fixed price consumer can’t participate in lower prices. Only the customer who opts for a capped price is shielded from higher prices, while being able to enjoy bargain prices. The capped consumer elects superior (and the only truly effective) coverage and not surprisingly, there is a higher price, i.e., cap premium add-on, associated with the best insurance available.

However, there are markets where homeowners rail against paying cap premiums and prefer to purchase “free” fixed price half protection rather than more expensive capped price full protection. Heating oil retailers in these markets must offer fixed price programs or forego selling to a possibly substantial segment of the customer base. In this circumstance, the dealer would be wise to obtain payment for all or most of the fixed price gallons up front or at least prior to the start of the heating season. If this is not possible for a sizable portion of the fixed price volume and there is a realistic possibility of falling prices, the seller has default risk.

Hedging Against Defaults: Out of the Money Call Options

An example illustrates this risk and how to hedge it. Let’s say that 200,000 gallons of pay-on-delivery, fixed price gallons are sold to consumers. Based on 2008/2009, the retailer estimates that if the price of heating oil falls $1.00, he is likely to experience defaults on 30% of this volume, which is 60,000 gallons. The goal is to hedge the 140,000 fixed price gallons that are not vulnerable to default and to hedge the 60,000 gallons of potential “involuntary, no premium caps” that carry downside risk for the seller. Hedging the 140,000 gallons is easy; purchasing wet barrel contracts on a heat curve will get the job done. Hedging the potential default gallons requires more creativity, and modeling tools at Hedge Solutions verify that a viable hedge is 20 cents out of the money call options. The following graphs capture this modeling:

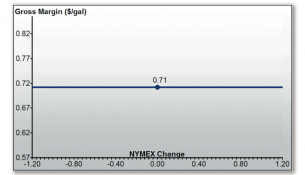

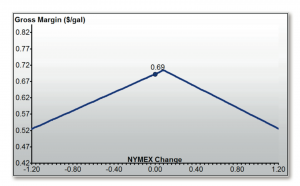

If a heating oil retailer sells 200,000 fixed price gallons to consumers, hedges these sales with 200,000 wet barrel contract gallons purchased from a supplier and experiences no consumer defaults, modeling shows the following program profitability profile. Note that margin is extremely stable, whether prices rise or fall.

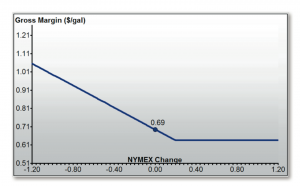

If, however, prices decline significantly and 30 percent of consumers default and refuse to take delivery of their fixed price gallons, the retailer’s profitability profile is altered as follows:

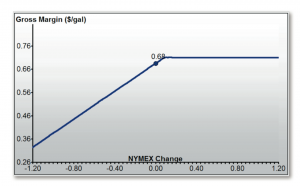

Since prices have presumably fallen at least $1.00, the retailer’s margin has been cut in half or worse. However, perhaps because the petroleum products market showed signs of weakness, the retailer anticipated a price drop-off and the potential for defaults, so he hedged 70 percent of his fixed price sales with supplier wet barrel contracts and the remaining 30 percent with 20 cents out of the money call options. What does this strategy do to his profitability profile? The answer is:

This profile is considered quite acceptable. Margin in a falling market is 67 cents and stable and margin in a rising market is 63 cents and stable. The cost of the call options in this illustration is about 8 cents per gallon or $4,800 (less closer to the heating season and more further before the winter), is included in the modeling and cannot be passed on to customers as a cap fee.

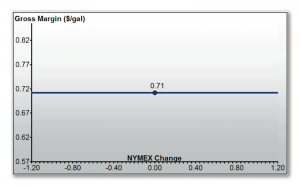

If you wonder what the profitability profile looks like if you cover potential defaults with 20 out call options and the defaults don’t occur, please note the following graph:

Hedging Against Defaults: Partially Unhedged Fixed Price Sales

If the retailer doesn’t want to bear the cost of 20-out call options, he can still hedge (sort of) against fixed price defaults. Consider for a moment that the most fundamental upside protection is a fixed price hedge and the most fundamental downside protection is no hedge. It’s going to be crude and imprecise, but a combination of these two approaches is another way to hedge against defaults. The following illustrates this hedging concept:

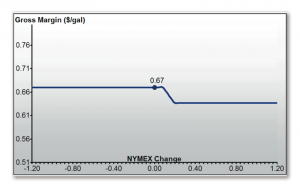

The heating oil retailer sells 200,000 fixed price gallons to consumers, hedges these sales with 168,000 wet barrel contract gallons purchased from a supplier, leaves the remaining 32,000 gallons of fixed price sales unhedged and experiences 30 percent defaults. Modeling shows the following program profitability profile:

At the current price, margin is 69 cents. If price goes up $1.20 or down $1.20, margin is 53 cents. That’s a 16 cents variation, which is not very good, but on the downside, it’s a lot better than the graph above (200K fixed price hedges, no default hedges, 60K [30 percent] defaults) where if price falls $1.20, the margin is 32 cents.

Summary

In summary, here are the alternatives for addressing the possibility of fixed price contract defaults, in order of preference: (1) Don’t sell fixed price gallons (caps price only); (2) Collect as much fixed price money as possible prior to the start of the heating season; (3) Hedge potential fixed price defaults with 20 cents out of the money call options; and (4) Leave some of the fixed price sales unhedged. How much unhedged? That can be difficult to determine without the benefit of a modeling tool, such as the proprietary software used by Hedge Solutions.